In What Ways Might Household Saving Rates Reflect the History of a Country?

Do you ever stop and wonder why people in some countries seem to save every penny, while others spend freely without a second thought? I mean, it’s not just about being rich or poor, it’s deeper than that. Household saving rates, basically the portion of income families set aside, can actually tell a story about a country’s history.

Think about it: if your grandparents lived through a war, hyperinflation, or a major economic crash, chances are they taught their kids to be careful with money. That cautious mindset often sticks, even decades later. Meanwhile, countries with solid social safety nets or steady economies might see people spending more because, well, they feel safe.

So, let’s dive into this. We’ll explore how a country’s past crises, culture, government policies and even the age of its population shapes the way households save today.

Understanding the Savings Rate

The savings rate is the ratio of personal savings to disposable personal income and can be calculated for an economy as a whole or at the personal level. The Bureau of Economic Analysis defines disposable income as all sources of income minus the tax you pay on that income.1 Your savings are disposable income minus expenditures, such as credit card payments and utility bills.

Using this approach, if you have $30,000 left after taxes (disposable income) and spend $24,000 in expenditures, then your savings are $6,000. Dividing savings by your disposable income yields a savings rate of 20% ($6,000 / $30,000 x 100).

A savings rate is determined by the degree of time preference either for an individual or as an average across a group of people. Time preference is the degree to which a person or group of people prefers current versus future consumption. The more someone prefers to consume goods and services now as opposed to in the future, the higher their time preference, and the lower their savings rate will be. Time preference is the fundamental economic cause of the observed savings rate.

1. Crises Leave a Mark You Can’t Ignore

Okay, let’s start with something obvious: crises, wars, depressions, hyperinflation leave a mark on people’s habits.

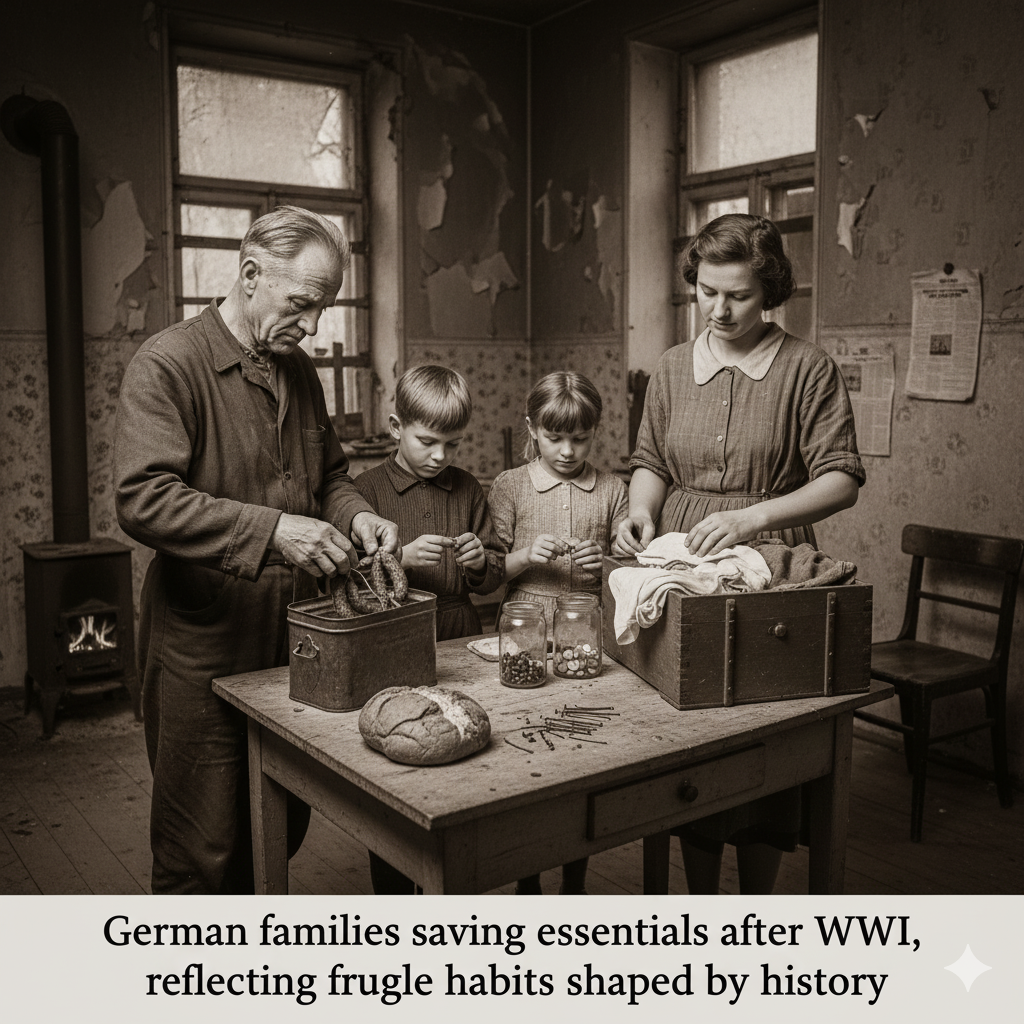

Take Germany after World War II, for example. Families had gone through scarcity and inflation. People saved everything they could, sometimes hoarding essentials like food, coal and even simple household items. Even after the economy recovered, this cautious approach stuck for generations.

Or look at Argentina in the 1980s. Hyperinflation forced families to think creatively. Cash was unreliable so people kept savings in foreign currency or bought gold. These habits did not just vanish when things got better they became cultural norms.

See, these behaviors are not just about money, they’re psychological. People who experience tough times learn lessons they pass down.

2. Government Policies Shape How We Save

Ever thought about how the government affects your personal savings? Yeah, it actually matters a lot. Taxes, interest rates, pensions all these things influence whether people save or spend.

High interest rates: When banks offer good returns, people save more. Makes sense right?

Strong pension systems: If the government promises a secure retirement, people might save less.

Tax incentives: Governments sometimes give tax breaks for retirement accounts, nudging people to save.

Take Japan, for instance. Their historically high saving rates were not just culture; they were encouraged by government policies, low-risk savings and incentives. Saving became the “smart” thing to do.

[OECD Household Savings Data]

(https://data.oecd.org/hha/household-savings.htm)

3. Culture Matters More Than You Think

Culture plays a huge role too. Some societies emphasize thrift, planning and family responsibility. Others? Well they love spending and borrowing.

East Asia: Confucian values emphasize frugality. It is not just practical, it is moral. You save for your family, for the future.

United States: Optimism and consumer culture encourage spending. People buy cars, houses and gadgets often on credit.

Extended families: In places where family supports each other financially individuals might save less because they rely on relatives.

4. Post-Crisis Booms Affect Spending Too

History shows that after tough times, booming economies can change saving patterns.

US in the 1950s: Post-WWII economic boom meant higher wages and more spending. But families are still saved for homes and education.

Germany’s Wirtschaftswunder: Their “economic miracle” after WWII combined prosperity with cautious saving. People were optimistic but remembered past hardships.

See the pattern? Saving is about fear, yes but also confidence and opportunity.

5. Financial Crises Leave Long-Term Habits

Crises aren’t just short-term annoyances; they leave long-term habits.

2008 Global Financial Crisis: Many households worldwide started saving more after seeing job losses, falling homes, and stock market crashes.

Argentina 2001–2002: Bank freezes and hyperinflation forced people to adopt extreme caution. Some families are still careful today. [World Bank on Savings and Economic Crises]

(https://www.worldbank.org/en/topic/financialsector/overview)

6. Demographics Reflect History**

Population age matters too. Older people tend to save more when they remember tough times. Younger generations? They’re often more willing to spend, especially if they grew up in stable economies.

Older populations: Higher savings rates due to past hardships.

Younger populations: Lower savings rates, often confident in the economy.

7. Modern Changes in Saving Behavior

With globalization, technology and easy credit, saving habits are changing fast. Even countries that historically saved a lot are seeing shifts.

China: High-saving society, but urban youth are spending heavily on tech, fashion and experiences.

India: Gold and bank savings are still popular, but digital wallets and online investments are growing.

It’s crazy how technology can shift centuries-old habits in just a few years.

Conclusion

Household saving rates aren’t just boring statistics, they are a window into a country’s history. Wars, crises, government policies, cultural values and demographics all leave their mark. Understanding savings gives insights into the past, helps predict the future and even explains why your own family handles money the way it does.

FAQs

Why do some countries save more than others?

It is a mix of history, culture, government policies and demographics.

Can saving habits change quickly?

Yes. Booms, recessions and new policies can shift saving rates in a few years.

How does culture affect saving?

Family traditions, frugality and long-term planning strongly influence savings.

Is high saving always good?

Not necessarily. Too much saving may indicate fear or economic insecurity; too little may reflect confidence or social support.

Where can I find data on household savings?

[OECD] (https://data.oecd.org/hha/household-savings.htm)

[World Bank] (https://www.worldbank.org/)

[IMF Reports] (https://www.imf.org/en/Publications/WP)